FAQs

Question1: Is it mandatory for companies who are established outside the EU to appoint a tax representative in France when the company achieved taxable sales or service income in France?

Question 2: How to choose a tax representative in France?

In particular, registered accountants or lawyers are not allowed to become a tax representative due to the special restriction of professional regulations.

Question 3. What is the designation procedure?

1. The name and address of the company and the legal representative

2. The consent of the tax representative to the designation;

3. The commitment by the tax representative to carry out the company’s VAT declaration and payment obligation;

4. The effective date of tax representative service (the appointment must be made prior to carrying out operations in France);

The above documents should be submitted by the tax representative to the taxation department to which they belong. The tax authority will notify the applicant in writing whether it is approved. Note: the company must appoint only one tax representative for all the operations it carries out in France.

Question 4: What are the obligations of the tax representative?

1. Issue invoices for the entrusted company with the identity of tax representative, they must indicate their fiduciary status. The entrusted company can also issue an invoice by itself, but it must indicate the name, address and VAT number of its tax representative.

2. Keep accounts of the operations carried out in France by the company. However, if the foreign company prefers to keep its own accounts, it must enable its tax representative can submit the accounting books and supporting documents relating to the transactions to the French local tax authorities;

3. File the turnover declarations and, where applicable, pay the VAT due by the represented company;

4. If applicable, to subscribe to the Declaration of Exchange of Goods (DEB) and the European Declaration of Services (DES) of the foreign taxable person.

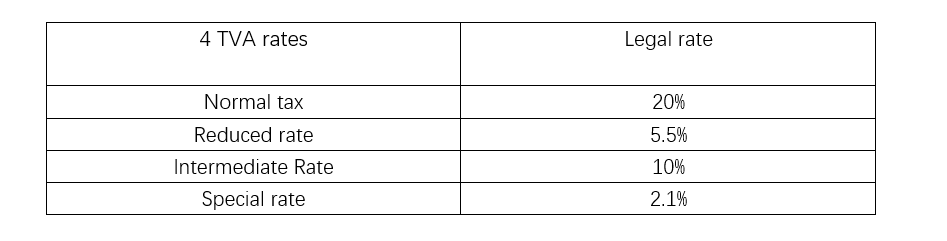

Question 5: Are all VAT rates in France 20%?

There are 4 different VAT rates in France. The standard VAT rate is 20%, applicable to all business and service activities that are not specifically stipulated by law. A reduced rate of 5.5% applies to certain goods and services that are mainly considered to be necessities, such as products intended for human consumption (with some exceptions). Books and sports tickets are also covered by this reduced rate. In addition, an intermediate rate fixed at 10% applies to certain goods and services, sales of food products for consumption on the spot and certain work relating to housing completed more than 2 years ago. Finally, a special rate of 2.10% is applicable in particular to reimbursable medicines and blood products.